產(chǎn)業(yè)資訊

產(chǎn)業(yè)資訊

醫(yī)藥魔方

醫(yī)藥魔方  2024-06-28

2024-06-28

500

500

近幾年,非腫瘤領(lǐng)域的臨床需求逐漸進入眾多制藥企業(yè)的視野粹懒,尤其是肥胖、代謝功能障礙相關(guān)脂肪性肝炎(MASH)顷级、炎癥性腸财榇尽(IBD)等疾病領(lǐng)域。其中伺罗,IBD作為西方國家的高發(fā)疾病寨衣,是制藥巨頭的重點關(guān)注對象。

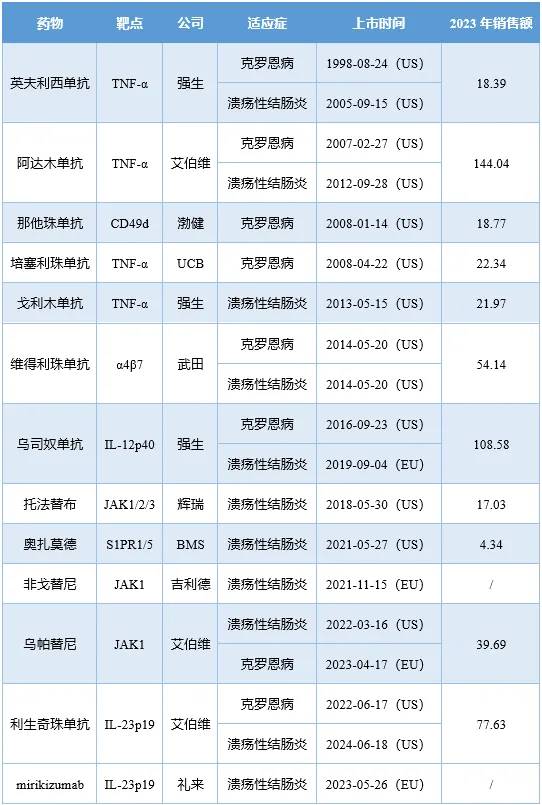

1998年奇巍,英夫利西單抗獲FDA批準用于治療克羅恩灿鐾小(CD),開啟了IBD的靶向治療之路含罪。如今26年光景過去笔广,IBD領(lǐng)域的創(chuàng)新靶向療法已多達13款,其中最暢銷藥物維得利珠單抗(主要適應(yīng)癥為IBD)的銷售額已超50億美元惠服。

獲批IBD適應(yīng)癥的靶向藥物(億美元)

注:維得利珠單抗的銷售額為自然年收入灿西。

疾病負擔的加重仍在推動IBD市場規(guī)模的擴大。目前全球約有600-800萬IBD患者[1,2]断猩,其中歐美國家IBD患者已超過500萬善婉。而中國的IBD發(fā)病率也在快速增長,2019年患者規(guī)模已達到91萬[3]肪瘤。據(jù)Transparency Market Research預測抄瓦,IBD市場規(guī)模到2030年將達到490億美元。

如此龐大的市場需求也吸引了眾多玩家入局陶冷。自2023年至今钙姊,IBD領(lǐng)域已達成23項交易,交易額總計超200億美元埂伦。

2023年至今IBD領(lǐng)域重大交易(億美元)

注:僅統(tǒng)計總交易額超1億美元的合作/收購交易

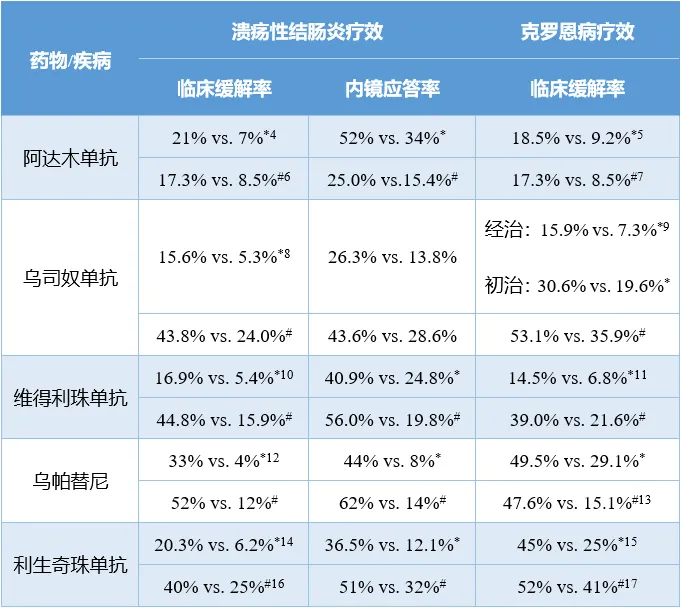

BD交易如火如荼進行的同時煞额,IBD領(lǐng)域的產(chǎn)品開發(fā)爭霸賽也高潮迭起。目前沾谜,阿達木單抗膊毁、烏司奴單抗、維得利珠單抗类早、烏帕替尼和利生奇珠單抗是在IBD領(lǐng)域激戰(zhàn)正酣的五大明星產(chǎn)品媚媒。

IBD領(lǐng)域五大明星產(chǎn)品療效一覽

注:1)阿達木單抗的潰瘍性結(jié)腸炎療效數(shù)據(jù)選自GAIN研究,因其同時納入了歐美人群涩僻;2)*為誘導治療數(shù)據(jù)缭召;#為維持治療數(shù)據(jù);3)以上研究的對照組均為安慰劑組逆日。

阿達木單抗憑借著至少7年的先發(fā)優(yōu)勢嵌巷,再加上在類風濕性關(guān)節(jié)炎、銀屑病關(guān)節(jié)炎和強直性脊柱炎三項自免適應(yīng)癥上的市場滲透經(jīng)驗芭贬,搶占IBD市場份額算是輕車熟路恋都。但是在維得利珠單抗上市之后,阿達木單抗在IBD領(lǐng)域的地位開始下降坚呜。因為anti-α4β7提供了更強的靶向治療效果[18]程伞,維得利珠單抗在針對UC的頭對頭研究中成功擊敗了阿達木單抗[19]。

靶向IL-12/IL-23的烏司奴單稍晚一些加入戰(zhàn)局闸虹,試圖沖擊IBD藥物的市場格局暴既。不過,相比于前兩款產(chǎn)品敌痴,烏司奴單抗針對IBD的治療效果并未有明顯提升磁饮,這恐怕也是其銷售額在獲批CD適應(yīng)癥后未大幅上升的原因之一。遺憾的是溪臊,其挑戰(zhàn)阿達木單抗的III期SEAVUE研究也以失敗告終[20]减少。

作為自免疾病賽道的領(lǐng)軍企業(yè),強生在IL-23靶點上推陳出新和鞏固優(yōu)勢镊鹊。新一代產(chǎn)品古塞奇尤單抗在IBD領(lǐng)域也交出一份滿意的答卷填抬。今年4月,古塞奇尤單抗對比烏司奴單抗治療CD的兩項頭對頭研究大獲成功隧期,而其誘導治療和維持治療UC的III期QUASAR研究也順利達到主要終點痴奏。IBD的戰(zhàn)局迎來一個實力選手。

艾伯維的當家產(chǎn)品阿達木單抗失去市場獨占期厌秒,但接棒產(chǎn)品烏帕替尼已經(jīng)成長起來读拆。在IBD的適應(yīng)癥上,無論是誘導治療還是維持治療鸵闪,烏帕替尼對CD和UC均有著超群的治療效果檐晕。口服的獨特優(yōu)勢也讓其在市場競爭中如虎添翼蚌讼。上市第5年辟灰,烏帕替尼的年銷售額已接近40億美元。利生奇珠單抗是艾伯維在IBD領(lǐng)域的另一個籌碼篡石,該產(chǎn)品已在頭對頭研究中打敗烏司奴單抗芥喇。

從臨床數(shù)據(jù)來看西采,烏帕替尼、利生奇珠單抗和古塞奇尤單抗在IBD上的療效范圍接近继控,未來幾年IBD領(lǐng)域的戰(zhàn)況也將是這三款產(chǎn)品主導眠便。

3款產(chǎn)品療效一覽

注:1)*為誘導治療數(shù)據(jù);#為維持治療數(shù)據(jù)况饥;2)除紅色標注數(shù)據(jù)的對照組為烏司奴單抗外其便,其余研究的對照組均為安慰劑。

IBD作為市場規(guī)妮┟埃可觀的自免疾病之一蘑杭,難免會讓藥企趨之若鶩,包括靶向IL-23的藥物競爭也著實激烈扬饰。除了艾伯維和強生在這一賽道雙龍際會宛办,禮來的IL-23單抗mirikizumab正迎頭趕上,還有多款國產(chǎn)IL-23靶向藥物對國內(nèi)IBD市場虎視眈眈班跟。競爭激烈如斯菱计,同賽道玩家阿斯利康已及時止損。

國產(chǎn)IL-23靶向藥物在研情況

臨床需求尚未得到充分滿足的IBD領(lǐng)域已成為藥企擴張自免業(yè)務(wù)版圖的不二選擇虹婿,其戰(zhàn)況已有日益焦灼之勢壤生。自英夫利西單抗上市以來,靶向TNF-α朝刊、IL-12耀里、IL-23等炎癥因子的療法已統(tǒng)治IBD領(lǐng)域二十多年,不過這種局面正在發(fā)生改變拾氓。去年7月冯挎,默沙東高價收購Prometheus Biosciences讓TNF樣配體1A(TL1A)靶點開始進入IBD玩家的視野。目前該賽道已達成4項授權(quán)/收購交易咙鞍,總交易額超200億美元房官,熱度矚目。未來续滋,IBD領(lǐng)域的市場之戰(zhàn)也將有TL1A抗體的一席之地翰守。國內(nèi)藥企諸如康方生物、信達生物疲酌、恒瑞醫(yī)藥等也在奮力加入戰(zhàn)局蜡峰。未來這個賽道將碰撞出怎樣的火花,且拭目以待吧朗恳。

參考資料

[1] The epidemiology of inflammatory bowel disease: East meets West.

[2] The four epidemiological stages in the global evolution of inflammatory bowel disease.

[3] Landscape and predictions of inflammatory bowel disease in China: China will enter the Compounding Prevalence stage around 2030.

[4] Adalimumab Induction Therapy for Crohn Disease Previously Treated with Infliximab.

[5] Adalimumab for induction of clinical remission in moderately to severely active ulcerative colitis: results of a randomised controlled trial.

[6] Adalimumab Induces and Maintains Clinical Remission in Patients With Moderate-to-Severe Ulcerative Colitis.

[7] Adalimumab induces and maintains clinical remission in patients with moderate-to-severe ulcerative colitis.

[8] Ustekinumab as Induction and Maintenance Therapy for Ulcerative Colitis.

[9] Ustekinumab as Induction and Maintenance Therapy for Crohn’s Disease.

[10] Vedolizumab as Induction and Maintenance Therapy for Ulcerative Colitis.

[11] Vedolizumab as induction and maintenance therapy for Crohn's disease.

[12] Upadacitinib as induction and maintenance therapy for moderately to severely active ulcerative colitis: results from three phase 3, multicentre, double-blind, randomised trials.

[13] Upadacitinib Induction and Maintenance Therapy for Crohn’s Disease.

[14] Risankizumab Induction Therapy in Patients With Moderately to Severely Active Ulcerative Colitis: Efficacy and Safety in the Randomized Phase 3 INSPIRE Study.

[15] Risankizumab as induction therapy for Crohn's disease: results from the phase 3 ADVANCE and MOTIVATE induction trials.

[16] 艾伯維新聞稿. https://www.prnewswire.com/news-releases/risankizumab-skyrizi-met-primary-and-key-secondary-endpoints-in-52-week-phase-3-maintenance-study-in-ulcerative-colitis-patients-301851542.html.

[17] Risankizumab as maintenance therapy for moderately to severely active Crohn's disease: results from the multicentre, randomised, double-blind, placebo-controlled, withdrawal phase 3 FORTIFY maintenance trial.

[18] https://www.entyviohcp.com/mechanism-of-action.

[19] Vedolizumab versus Adalimumab for Moderate-to-Severe Ulcerative Colitis.

[20] Ustekinumab versus adalimumab for induction and maintenance therapy in biologic-naive patients with moderately to severely active Crohn's disease: a multicentre, randomised, double-blind, parallel-group, phase 3b trial.

[21] The Efficacy and Safety of Guselkumab Induction Therapy in Patients With Moderately to Severely Active Ulcerative Colitis: Results From the Phase 3 QUASAR Induction Study.

[22] 強生新聞稿. https://www.businesswire.com/news/home/20201012005149/en/TREMFYA%C2%AE%E2%96%BC-guselkumab-Induces-Clinical-and-Endoscopic-Improvements-in-Patients-with-Moderately-to-Severely-Active-Crohn%E2%80%99s-Disease-based-on-Interim-Results-from-Phase-2-Study.

[23] 強生新聞稿. https://www.jnj.com/media-center/press-releases/tremfya-guselkumab-quasar-maintenance-study-in-uc-met-its-primary-endpoint-and-all-major-secondary-endpoints-including-highly-statistically-significant-rates-of-endoscopic-remission.

[24] 強生新聞稿.https://www.jnj.com/media-center/press-releases/tremfya-guselkumab-demonstrates-superiority-versus-stelara-ustekinumab-in-phase-3-crohns-disease-program.

產(chǎn)業(yè)資訊

深藍觀 2024-11-28

21

產(chǎn)業(yè)資訊

深藍觀 2024-11-28

21

產(chǎn)業(yè)資訊

瞪羚社 2024-11-28

25

產(chǎn)業(yè)資訊

瞪羚社 2024-11-28

25

產(chǎn)業(yè)資訊

丹諾醫(yī)藥 2024-11-28

24

產(chǎn)業(yè)資訊

丹諾醫(yī)藥 2024-11-28

24

微信公眾號

微信公眾號 熱門資訊

熱門資訊 熱點標簽

熱點標簽